Welcome to the email list.

Check your inbox for a short note from Ben & David.

Something didn't quite work out. Try again?

This episode on Acquired

EMAIL PREVIEW — We got to try our hand at inking and painting animation cel’s on our trip to Disney’s animation headquarters!

This episode on Acquired

No items found.

No items found.

China's Social Commerce Phenomenon

overview

We kick off Season 7 with a bang: Pinduoduo, the incredible five year-old Chinese mashup of "Costco and Disneyland" (as self-described in their IPO prospectus) which recently became the fastest company ever to pass $100B market capitalization. What makes PDD so special, and how were they able to enter a market that everyone considered "already won" and disrupt massive entrenched competitors Alibaba and JD.com? This story is chock-full of lessons that apply not only to China tech, but to high-growth company building and investing everywhere.

More on the episode

Links

- Photo of 26 year-old Colin at lunch with Warren Buffett: https://thelowdown.momentum.asia/cv-of-pinduoduos-founder/

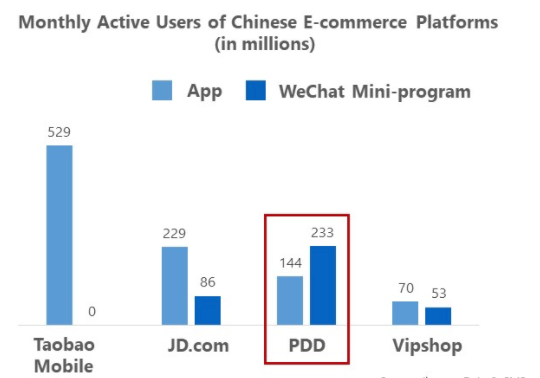

- PDD users on mini-programs vs other Chinese e-commerce players: https://miro.medium.com/max/1080/0*39fpSP_JqhDaPhQ2.png

Carve Outs

- How to Make a Spaceship https://www.amazon.com/How-Make-Spaceship-Renegades-Spaceflight/dp/1594206724

- Creativity, Inc. https://www.amazon.com/Creativity-Inc-Overcoming-Unseen-Inspiration/dp/0812993012

corrections

Note: Acquired hosts and guests may hold assets discussed in this episode. This podcast is not investment advice, and is intended for informational and entertainment purposes only. You should do your own research and make your own independent decisions when considering any financial transactions.

Welcome to the email list.

Check your inbox for a short note from Ben & David.

Something didn't quite work out. Try again?

Pinduoduo

S7

•

Jul 16, 2020

1

x

{kind=link}